Research

7 min read

Real Yield Is Replacing Inflationary Yield in Institutional Staking

The fee-based yield curve takes shape.

Published on

May 11, 2026

Introduction

For most of crypto's history, staking yield was paid with new supply, leaving holders to absorb the dilution as the cost of participation. The model worked while ecosystems were small and growth was the only metric that mattered. In 2026, that model is being replaced. Five major partner networks have restructured validator income away from token issuance and toward a share of real network revenue.

With Bitwise's second amended S-1 for a spot HYPE ETF (BHYP ticker) filed on April 10, 2026, including a staking mechanism that passes roughly 85% of rewards to shareholders, and the SEC and CFTC formally classifying major crypto assets as digital commodities on March 17, 2026, the demand-side push has finally met a supply-side answer. What looks like a series of unrelated governance updates is the formation of a yield curve that institutional allocators can finally model.

The problem with inflationary yield is not the yield

Asset allocators do not reject inflationary staking because the headline number is too low. They reject it because the number is hard to model. Inflationary yield is paid in a token whose supply is, by definition, growing at the rate of the yield itself. That makes the asset behave less like a fixed-income claim and more like a leveraged bet on appreciation.

For ETF sponsors and treasury allocators evaluating staking under traditional asset-allocation frameworks, the holder is paid in the same currency being diluted to pay them. The accounting outcome resembles share-based compensation more than coupon income, and that distinction matters when an allocator has to slot the position into a fixed-income mandate, a duration bucket, or an audited yield disclosure.

How fee-distribution staking actually works

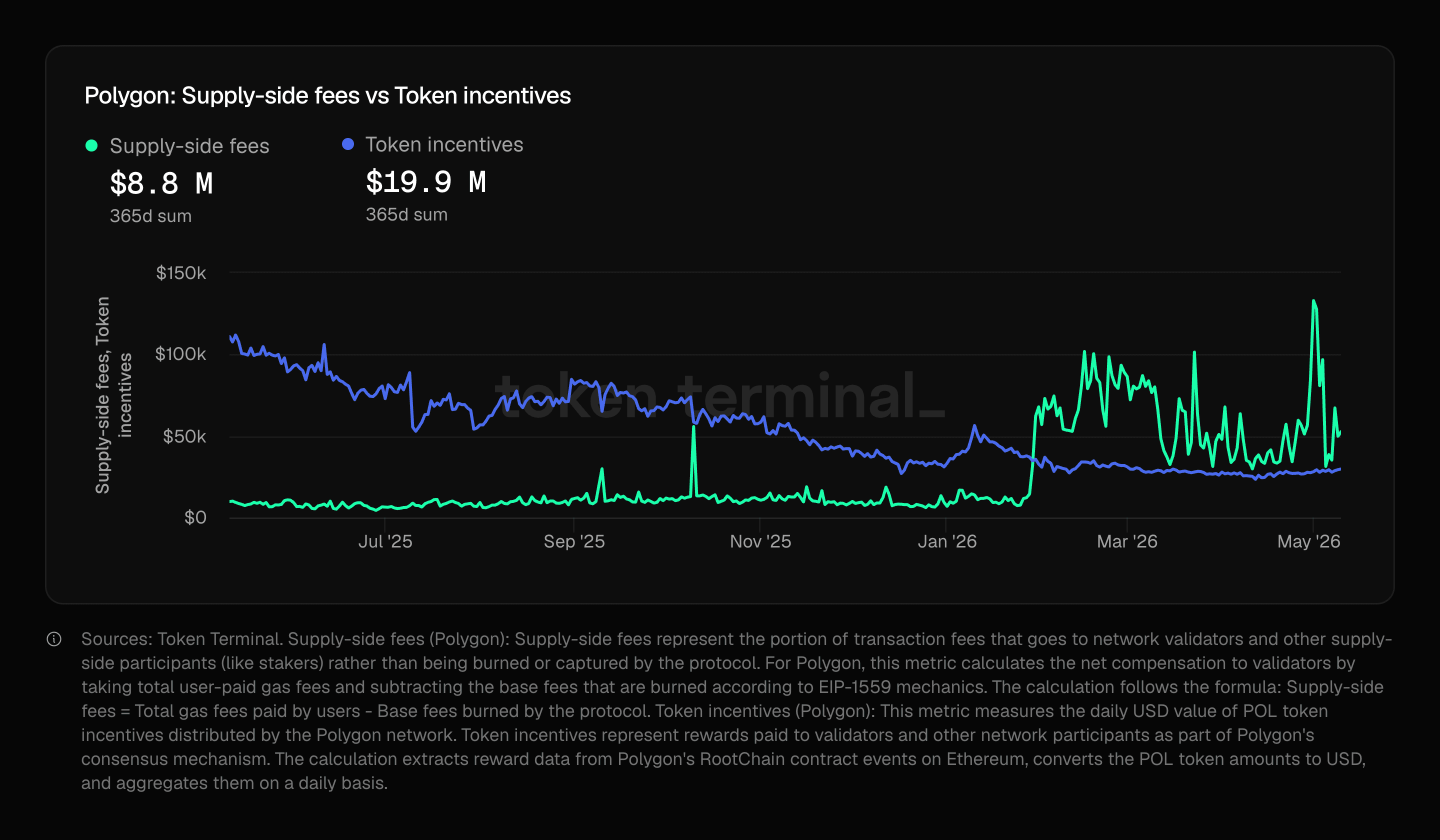

A fee-distribution model routes the revenue a network already generates from transactions directly to the entities securing the chain. The cleanest live case study is Polygon.

Polygon's transition toward fee-based validator income accelerated after the October 2025 Rio upgrade introduced PIP-65, enabling EIP-1559 priority fees to be distributed across the validator set under the new VEBloP architecture. While the mechanism went live in October, distributions only began ramping meaningfully from December onward.

The real inflection came in late January 2026, when Polygon processed nearly 3.9 billion monthly transactions and blockspace demand intensified sharply. As users and bots competed for inclusion, priority fees rose dramatically, causing validator fee revenue to surge.

Because Polygon burns base fees under EIP-1559, Token Terminal's "supply-side fees" metric increasingly reflected this growing priority fee economy. By February 2026, there was a sustained inversion of inflation and fee-based validator income on the network, marking one of Polygon's clearest shifts toward transaction-driven staking yield.

The pending PIP-85 builds on this architecture by routing 50% of validators' share directly to POL stakers via monthly merkle claims integrated into the staking UI, replacing the current dependency on validators choosing to share rewards with their delegators (Polygon Governance Portal, April 2026).

Similar transitions are visible across other partner networks, each with a different architectural answer:

- Hyperliquid allocates 97% of protocol trading fees to its Assistance Fund, which conducts open-market HYPE buybacks, with $52.7M in retained revenue over 30 days (DefiLlama, April 2026).

- TRON's fee architecture passes roughly $30.6M in monthly chain fees through to validators and stakers with no protocol burn diluting validator economics (DefiLlama, April 2026).

- NEAR began executing its disinflationary roadmap on October 30, 2025, reducing issuance from 5% toward a 2.5% target and removing roughly 60 million tokens of annual supply (NEAR Governance, 2025).

- Canton Network's first halving in January 2026 cut maximum issuance by 50% and shifted reward weight toward App Rewards at 62%, with Super Validator rewards reduced from 48% to 20% to incentivize utility over liveness.

The staked position resembles a claim on transaction fees rather than a hedge against dilution, and yield can be benchmarked against on-chain volume rather than a token's supply schedule.

Why the shift is concentrated in this quarter

The simultaneity is the signal. Five major partner networks moved on the same idea inside two quarters, and the timing aligns with the regulatory unlocks above. Together, these widen the institutional buyer base from custodial trading desks to ETF sponsors, treasuries, and bank-affiliated mandates, all operating under fiduciary frameworks that demand yield denominated in operating revenue, not token issuance. What appears as a wave of unrelated upgrades is the protocol layer adapting to a new class of marginal buyer.

The tradeoff embedded in real-yield models

The design carries a second-order question worth watching. When yield is paid from fees and the staked asset becomes scarcer through buybacks, the same asset must do two jobs at once: hold value, and circulate enough to generate the fees that fund the yield. Monetary economists have written about this tension between store of value and medium of exchange for more than a century. The classic formulation, often attributed to Gresham, is that good money is hoarded while inferior money circulates.

The architectural answer matters. Networks like Hyperliquid, which separate staking (HYPE) from settlement (USDC), sidestep the tension by design: the asset that captures yield is not the asset that pays for transactions. Networks where a single token serves as both staked asset and gas currency face it more directly, and the question for allocators is whether the network's incentive design can hold the balance between scarcity and circulation. The design choice is part of the long-term yield thesis.

What this means for institutional allocators

When validator income is denominated in network revenue rather than new supply, staking begins to look like an infrastructure asset class. The closest traditional analog is operating income from a regulated utility, where revenue scales with usage and the holder's claim is on real economic activity. Allocators can model that, compare it to bond yields, and underwrite the asset under the frameworks they already use.

The result is a yield curve with discernible quality tiers: networks with high fee throughput and sustainable circulation at the top, networks still subsidizing yield through emissions at the bottom. The first tier is the asset class institutions will model first, allocate to first, and benchmark against. That ordering decides where the capital goes, and which validator operators benefit from the inflow.

FAQ

What does real yield mean in institutional staking?

Yield paid from network transaction fee revenue rather than new token issuance, treating validators and delegators as receivers of usage-based rent.

Why does it matter for ETF sponsors and treasuries?

Fee-based yield resembles operating income from a regulated utility, fitting traditional asset-allocation frameworks. Inflationary yield does not, which is why it has historically been hard to underwrite at institutional scale.

Which networks are leading the shift?

Polygon, Hyperliquid, TRON, Canton Network, and NEAR have each restructured validator income toward fee revenue or supply discipline within the past two quarters, each using a different architectural mechanism.

Is fee-based yield sustainable over time?

Sustainability depends on whether the staked asset and the transaction currency are the same token. Architectures that separate the two, like Hyperliquid's HYPE-USDC model, preserve the fee base as the staked asset becomes scarcer through buybacks.

About Luganodes

Luganodes is a world-class, non-custodial blockchain infrastructure provider that has rapidly gained recognition in the industry for offering institutional-grade services. It was born out of the Lugano Plan B Program, an initiative driven by Tether and the City of Lugano. Luganodes maintains an exceptional 99.9% uptime with round-the-clock monitoring by SRE experts. With support for 45+ PoS networks, it ranks among the top validators on Polygon, Polkadot, Sui, and Tron. Luganodes prioritizes security and compliance, holding the distinction of being one of the first staking providers to adhere to all SOC 2 Type II, GDPR, and ISO 27001 standards as well as offering Chainproof insurance to institutional clients.

The information herein is for general informational purposes only and does not constitute legal, business, tax, professional, financial, or investment advice. No warranties are made regarding its accuracy, correctness, completeness, or reliability. Luganodes and its affiliates disclaim all liability for any losses or damages arising from reliance on this information. Luganodes is not obligated to update or amend any content. Use of this at your own risk. For any advice, please consult a qualified professional.